How Much Down Payment Do You Actually Need to Buy a Home?

Quick Answer: Contrary to popular belief, most buyers do not need 20% down to purchase a home. Conventional loans can require as little as 3 to 5% down, FHA loans require 3.5%, and VA and USDA loans can require zero down for eligible buyers. Washington State also offers down payment assistance programs through the Washington State Housing Finance Commission that many buyers have never heard of.

A Myth That Keeps Buyers on the Sidelines

One of the most common things I hear from buyers who feel stuck is, "I just don't have enough saved yet." When I ask a follow-up question, it usually turns out they're estimating based on the 20% down payment rule, a number that's been repeated in real estate conversations for decades.

Here's the truth: 20% down has real advantages, but it is absolutely not a requirement for most buyers.

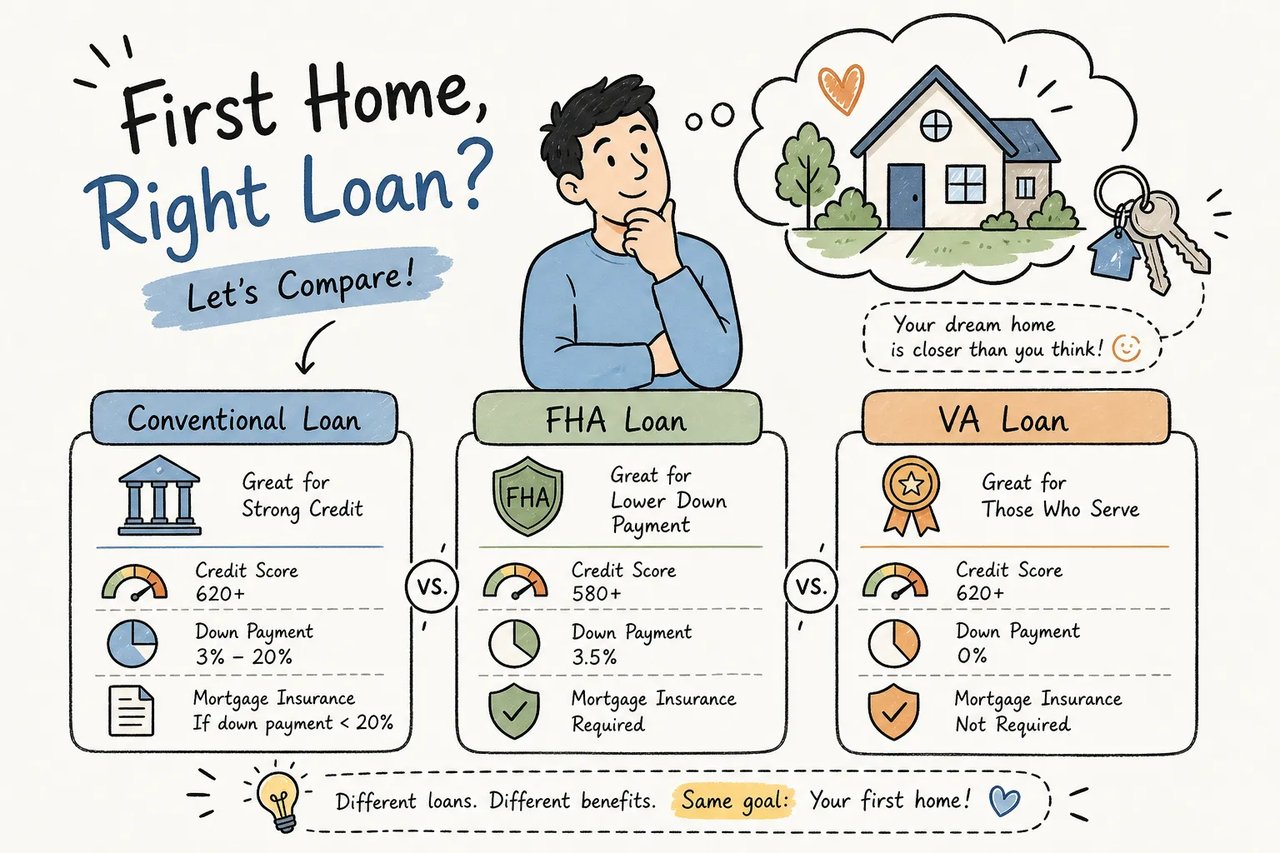

What Down Payments Actually Look Like Today

Conventional loans can require as little as 3 to 5% down for qualifying buyers.

FHA loans require 3.5% down and offer more flexible credit requirements, making them a common path for first-time buyers.

VA loans, available to eligible veterans and active service members, often require zero down.

USDA loans, available in qualifying rural and semi-rural areas, including parts of Skagit and Island County, can also require zero down.

If you've been saving toward 20% on a home priced at $500,000, that's $100,000. The same purchase under an FHA loan could require closer to $17,500. That's a significant difference, and it might mean you're already closer to buying than you realized.

Washington State Down Payment Assistance

Beyond loan program minimums, Washington State offers down payment assistance through the Washington State Housing Finance Commission. These programs can include grants that don't need to be repaid, forgivable second loans, and matched savings programs, depending on your income and the program's specific requirements.

Many buyers never explore these options simply because they don't know they exist. It's worth asking a lender directly whether you qualify before assuming you don't.

The Trade-Offs Worth Understanding

A lower down payment isn't free of considerations. Putting down less than 20% on a conventional loan typically means paying private mortgage insurance until you've built enough equity, and you'll carry a larger loan balance overall. These are real factors, and I'll walk through them honestly with every buyer rather than glossing over the downside.

But here's the core point: many buyers are sitting on the sidelines saving toward a number that simply isn't required. If the actual number you need is significantly lower than the one you've been working toward, that's information worth having sooner rather than later.

The Only Way to Know for Sure

A calculator app or a rule of thumb from a friend isn't going to give you an accurate picture. The only reliable way to know what you actually need is a real conversation with a lender who looks at your specific income, credit, and savings, and tells you honestly what's possible right now.

I work with lenders I trust precisely because they give straight, honest answers rather than just the number a buyer wants to hear. If you walk in assuming you need $80,000 and the real number turns out to be $30,000, I want you to know that as early as possible.

What This Means Locally

Across Snohomish, Skagit, and Island Counties, down payment assistance and low down payment loan programs can make a meaningful difference, particularly for first-time buyers trying to compete in areas like Lake Stevens or Edmonds where prices run higher. Skagit and Island County buyers may find these programs stretch even further given relatively lower price points.

Frequently Asked Questions

Do I really need 20% down to buy a house? No. Most buyers use loan programs requiring far less, ranging from 3 to 5% down for conventional loans, 3.5% for FHA loans, and potentially zero down through VA or USDA loans for those who qualify.

What down payment assistance programs are available in Washington State? The Washington State Housing Finance Commission offers several programs, including grants, forgivable second loans, and matched savings programs. Eligibility depends on income and other program-specific requirements, so checking directly with a lender is the best next step.

Is it better to put down more than the minimum required? A larger down payment reduces your loan balance and may eliminate mortgage insurance, but it also means tying up more cash upfront. Whether that trade-off makes sense depends on your overall financial picture and goals.

What is private mortgage insurance and will I have to pay it? Private mortgage insurance, or PMI, is typically required on conventional loans with less than 20% down. It protects the lender, not the buyer, and can usually be removed once you've built enough equity in the home.

Let's Find Out What You Actually Qualify For

Don't let an assumption about down payments keep you out of the market longer than necessary. I'd be glad to connect you with a lender who will give you a clear, honest picture of where you actually stand.

Renee Pilchard is the Managing Broker and owner of Pilchard Properties, affiliated with Realty One Group Orca, serving Snohomish, Skagit, and Island Counties.

Reach out for a referral to a trusted lender and an honest conversation about your real numbers.