Wondering how to buy a larger home in Lake Stevens without creating a stressful overlap with the home you still need to sell? You are not alone. Many move-up buyers are trying to balance more space, changing monthly costs, and tight timing all at once. The good news is that with a clear plan, you can reduce risk, protect your equity, and make smarter decisions before you commit. Let’s dive in.

Why timing matters in Lake Stevens

If you are moving up in Lake Stevens, timing is not just a convenience issue. It can affect your financing, your negotiating power, and how much pressure you feel during the move. In a market with limited inventory, small timing mistakes can become expensive.

Snohomish County had 2.04 months of inventory in March 2026, which is still below the 4 to 6 months often viewed as a balanced market. At the same time, the broader NWMLS service area reached 3.44 months of inventory in May 2026, showing that conditions are improving but are not fully relaxed. For you, that means options may be opening up, but careful planning still matters.

The median sales price in Snohomish County was $738,000 in March 2026. If you plan to use your current equity to help buy a larger home, your sale proceeds can play a major role in what you can comfortably afford next. That is why your sale and purchase need to work together as one strategy, not two separate transactions.

Start with your monthly payment

It is easy to focus on the list price of the next home. A better place to start is your full monthly housing cost. When you move up, even a modest jump in loan balance can change your payment faster than many buyers expect.

Freddie Mac reported the average 30-year fixed mortgage rate at 6.49% on June 25, 2026. At that rate, a larger mortgage can have a noticeable impact on your budget. Looking at payment first helps you stay grounded when comparing homes with extra bedrooms, larger lots, or updated features.

Your budget should also include more than principal and interest. As you compare options, remember to account for property taxes, insurance, closing costs, moving expenses, repairs, home improvements, and any HOA dues that may apply. If the larger home also means new furniture or projects after move-in, build that into your plan early.

Selling first is often the cleaner path

For many move-up buyers, selling first is the simplest and safest sequence. That approach can turn your existing equity into a down payment and lower the odds that you will carry two mortgage payments at the same time. It also gives you a clearer idea of your real budget instead of relying on estimates.

This path can feel less exciting because you may need temporary flexibility while you shop for the next home. Still, it often reduces financial pressure and gives you stronger footing when you write an offer. In a market like Lake Stevens, that clarity can be worth a lot.

Selling first also helps you understand your net proceeds more accurately. In Washington, the seller usually pays the real estate excise tax, and Lake Stevens has a 0.50% local REET on top of the graduated state rate. On a sale around the Snohomish County median, the combined state and local REET is about $13,136, which is a meaningful expense to plan for before you count on your equity.

Buying before you sell can work with planning

Sometimes the right larger home shows up before your current home sells. If that happens, you may have financing options that help bridge the gap. The key is understanding both the opportunity and the risk before you move forward.

Home equity financing is one possible tool. A home equity loan gives you a lump sum secured by your current home, while a HELOC lets you borrow against your equity as needed. Because both are secured by your property, falling behind on payments can put your home at risk, so this is not a casual decision.

If you are thinking about this route, the most important step is to review the numbers carefully before you make an offer. You want to know what you can carry if your current home takes longer to sell than expected. A larger home should feel like a smart next step, not a strain.

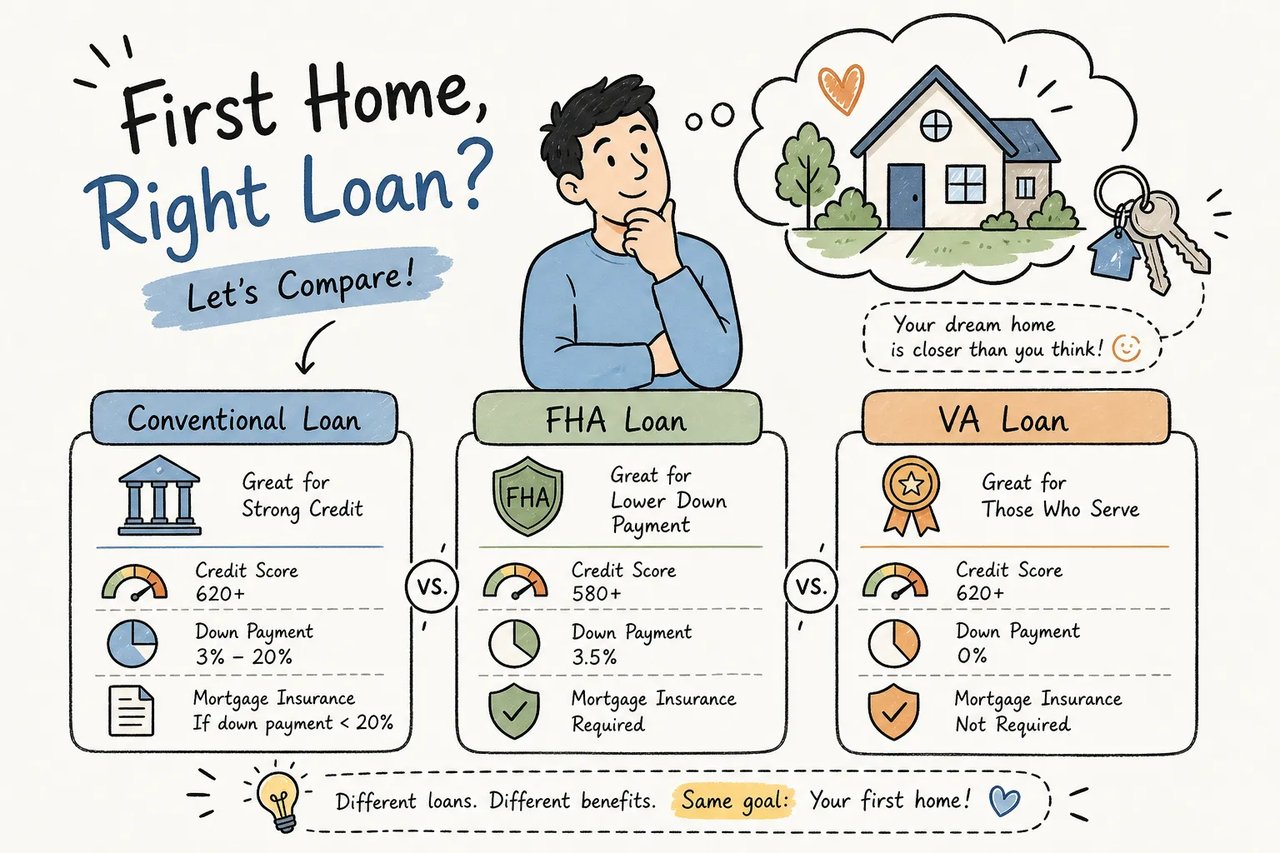

Preapproval is useful, but not final

Before you shop seriously, get preapproved and compare lender options. A preapproval letter can help you understand your likely borrowing range, but it is based on assumptions and is not a guaranteed loan offer. Rates can also change daily, which means your buying power may shift while you search.

It is smart to request Loan Estimates from multiple lenders so you can compare costs, not just rate headlines. Down payment size matters too. A 20% down payment can improve approval odds, while a smaller down payment may require mortgage insurance.

For move-up buyers, this step is especially important because your next purchase often depends on proceeds from your current sale. If your home sells for a little more or less than expected, your loan structure may change. That is another reason to treat the buy-and-sell process as one coordinated plan.

Use contingencies to reduce risk

When you need to buy and sell at nearly the same time, contingencies can help protect you. They are one of the main tools for managing uncertainty in a move-up purchase. The right structure can give you more control if financing, inspections, or your current sale do not line up exactly as hoped.

Common protections include financing and inspection contingencies. If your move depends on selling your current home, a home sale contingency may give you time to sell before closing on the next property. A home close contingency may give you time to complete that sale before you finalize the purchase.

These terms can make a big difference, but they also affect how a seller views your offer. A seller may continue showing the property, and a kick-out clause may allow them to accept a stronger noncontingent offer if one appears. That does not mean contingencies are a bad idea. It means you should use them strategically and understand the tradeoffs.

Build a buffer into your closing timeline

Even when everything looks aligned, closings are detail-heavy and timing can shift. Financing paperwork is not truly done until the end of the process. That is why back-to-back closings on the same day can create unnecessary pressure.

Borrowers must receive the Closing Disclosure three business days before closing. You should compare it with the earlier Loan Estimate and review your closing documents in advance. Some fees cannot increase at all, while others are limited in how much they can rise, so reviewing those numbers ahead of time matters.

A small buffer between your sale and your purchase can give you room to solve last-minute issues without turning your move into a scramble. In practice, many successful move-up plans depend less on perfect timing and more on allowing enough margin for normal delays.

Consider rent-back if you need flexibility

If your current home sells before your next home is ready, a rent-back agreement may help. This can allow you to stay in your home for a short period after closing if the buyer agrees. For some households, that extra time can make the transition much smoother.

A rent-back is not automatic, and the terms need to be written carefully. The rental period, daily cost if any, and final move-out date should all be clear. If you are trying to avoid moving twice, this can be a practical tool worth discussing.

Plan around school boundaries early

If your move includes school-age children, do not leave boundary questions until the end. Lake Stevens School District has said enrollment for the 2026-27 school year is limited to students who live within district boundaries because of overcrowding. The district also says non-resident variances will not be approved.

That means school boundaries may directly affect where and when you move. Families should use the district’s SchoolSite Locator to confirm attendance areas for any home they are considering. Even if a property seems ideal, you want to verify the boundary details before you make a decision.

This is a good example of why a move-up purchase is not only about square footage. In Lake Stevens, your timeline, address, and closing sequence may all shape how smoothly the transition works for your household.

A smart move-up plan focuses on equity

At its core, buying a larger home while selling your current one is an equity-and-timing decision. Your existing home is often the engine that makes the next purchase possible. Protecting that equity and giving yourself enough flexibility is usually more important than chasing the fastest possible timeline.

A strong plan often includes a few basics:

- A clear monthly payment target

- A realistic estimate of net sale proceeds

- A review of REET and other closing costs

- A financing backup plan if the next home appears first

- Contingencies that match your risk tolerance

- A closing timeline with some breathing room

- Early verification of school boundaries if needed

When you approach the process this way, you can make decisions with more confidence. You are not just buying a bigger house. You are coordinating two major transactions in a way that supports your budget, your move, and your next chapter.

If you are thinking about moving up in Lake Stevens, working with a local team that understands Snohomish County timing, pricing, and negotiation can make the process much more manageable. When you are ready to map out your options, connect with Pilchard Properties.

FAQs

How does the Lake Stevens market affect move-up buyers?

- Snohomish County had 2.04 months of inventory in March 2026, which means the market still requires careful timing even though broader inventory trends have improved.

What costs should you budget for when buying a larger home in Lake Stevens?

- You should plan for mortgage payments, property taxes, insurance, closing costs, moving expenses, repairs, home improvements, HOA dues if applicable, and seller costs such as Washington REET.

Should you sell your current home before buying a larger home in Lake Stevens?

- Selling first is often the cleaner path because it lets you convert equity into a down payment and reduces the chance of carrying two mortgages at once.

What financing options can help you buy before your current home sells?

- Possible options include a home equity loan or HELOC, both of which let you borrow against your current home’s equity but also carry risk because your home secures the debt.

What contingencies can protect you when buying a larger home while selling?

- Financing, inspection, home sale, and home close contingencies can help reduce risk by giving you protections if your loan, inspection, or current sale does not line up as planned.

Why should Lake Stevens buyers verify school boundaries early?

- Lake Stevens School District says enrollment is limited to students living within district boundaries for the 2026-27 school year, and non-resident variances will not be approved.