First-time home buyer assistance in Washington State is more extensive than most buyers realize, and far more accessible. Buying your first home here is expensive; that part is unavoidable. But the state has built a genuine system of financial support to help close the gap between renting and owning, and many buyers overlook available assistance simply because they assume they won't qualify.

The Washington State Housing Finance Commission, known as WSHFC, is the backbone of that system. It administers the majority of Washington homebuyer programs, from standard down payment assistance to specialized options for veterans, buyers with disabilities, and communities historically excluded from homeownership. The programs are real, the eligibility rules are specific, and the application process is learnable.

This article breaks down what's actually available, in plain language. By the end, you'll know which programs apply to your situation, what the income and eligibility rules actually mean, and what steps to take first.

What first-time home buyer assistance in Washington State actually covers

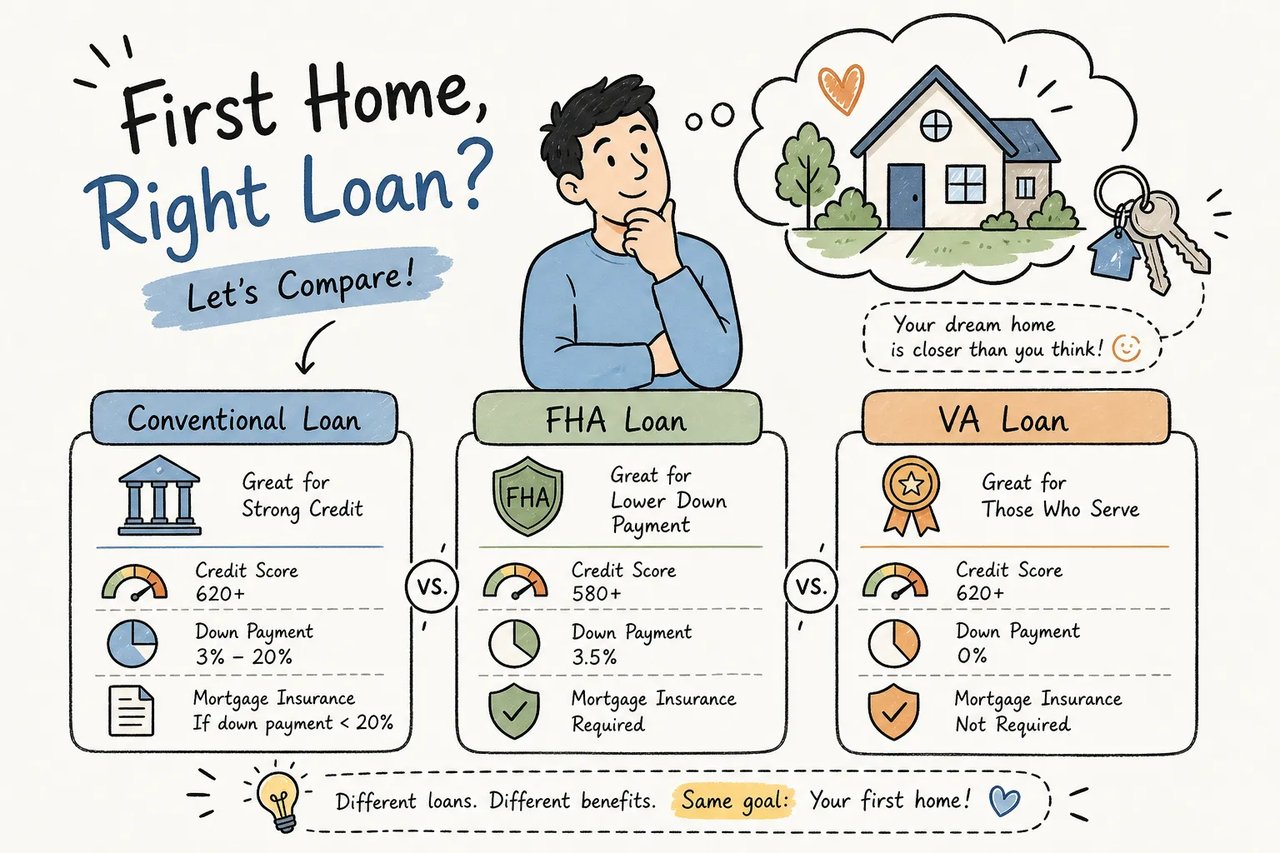

The WSHFC runs two primary first-mortgage programs: Home Advantage and House Key Opportunity. Both include a built-in down payment assistance component, which is where the real financial help lives. Understanding how that assistance is structured before you start shopping changes the entire conversation.

Home Advantage DPA: the program most Washington buyers use

Home Advantage is WSHFC's primary first-mortgage program and the most commonly used first-time buyer assistance option in Washington State. The down payment assistance is structured as a second mortgage at 0% interest, with no monthly payments. The amount is 3%, 4%, or 5% of the first mortgage loan, deferred until you sell the home, refinance, or reach 30 years of ownership. (Figures reflect current WSHFC Home Advantage program terms; verify current caps at wshfc.wa.gov.)

The household income cap is $215,000, which means a broad range of buyers qualify. For buyers in lower income brackets, there's a needs-based version: up to $10,000 at 1% simple interest, with income caps of $164,400 in King and Snohomish counties and $126,800 elsewhere. Neither version requires monthly payments on the assistance, which makes it functionally invisible during the life of the loan.

House Key Opportunity: the option for lower-income buyers

House Key is designed for buyers with lower household incomes, offering up to $15,000 in down payment assistance at 1% simple interest. Income eligibility ranges from roughly $100,000 to $175,000 depending on household size and county, check the WSHFC House Key Opportunity page for current figures by household size and location. Like Home Advantage, the loan is repaid upon sale or refinance, not through monthly installments.

The choice between the two programs comes down to income. If your household earns above the House Key threshold but below $215,000, Home Advantage is the right path. A WSHFC-approved lender can determine which program you qualify for based on your actual numbers.

Who qualifies for first-time home buyer assistance in Washington State

The first-time buyer definition most people get wrong

Under WSHFC rules, "first-time buyer" doesn't mean you've never owned a home. It means you haven't owned one in the past three years. That distinction reopens the door for many people who were homeowners at some point but have been renting since. In areas designated as targeted by the WSHFC, the three-year rule may also be waived entirely, expanding eligibility further.

How income limits work across Washington counties

Income limits are tied to Area Median Income and vary by county and household size. For Home Advantage, the statewide ceiling is $215,000 in gross household income. The needs-based DPA caps at $164,400 in King and Snohomish counties and $126,800 elsewhere. House Key's range runs from roughly $100,000 to $175,000 depending on household size and location.

Before checking program eligibility, calculate gross household income: all pre-tax earnings from every member of the household. Then check the current limits on the WSHFC website, where figures are updated annually based on HUD's published AMI data. For 2026 AMI values, visit wshfc.wa.gov or the HUD income limits page directly. You can also review a 2025 AMI limits analysis or the FY 2026 HUD income limits summary for additional context.

Credit score, property types, and lender requirements

Many participating lenders commonly require a minimum credit score of 620 for WSHFC programs, though WSHFC evaluates a borrower's full credit profile during underwriting. Eligible properties include single-family homes, condominiums, townhomes, and manufactured homes. Buyers must intend to occupy the property as a primary residence for at least three years and must work with a WSHFC-approved participating lender. Lenders also evaluate debt-to-income ratio during underwriting. If you need help assessing how much mortgage you can realistically afford, see Am I Taking On Too Much Debt Buying a Home?

Specialized programs most buyers overlook

Washington's assistance programs extend well beyond the standard options. Several specialized programs serve buyers in specific situations, and they often go unused because people simply don't know to ask.

The Covenant Homeownership Program: Washington's largest assistance option

The Covenant Homeownership Program is remarkable in its scope. Buyers who qualify can receive up to 20% of the home's purchase price, or a maximum of $150,000, plus closing costs, at 0% interest with deferred repayment. That is a significant sum, and it's one of the most underutilized first-time homebuyer grants Washington State offers. (See the WSHFC Covenant Homeownership Program page for current maximums and eligibility documentation.)

Eligibility is based on historical family ties to Washington. Qualifying buyers are those whose ancestors lived in Washington State before April 1968 and belonged to communities affected by racially restrictive housing covenants, including Black, Native American, Hispanic, Korean, Asian Indian, Native Hawaiian, and Pacific Islander individuals. Because the documentation process is more involved, the steps must happen in a specific order. Lenders upload historical records, birth certificates, school records, military records, or genealogical documents, and receive written WSHFC authorization before house-hunting begins. If you think your family history might qualify, this is the first call to make. For an overview, see the Covenant Homeownership Program page.

Veterans and disability assistance: additional programs worth checking

Veterans can access up to $10,000 in down payment assistance at 3% simple interest through the Veterans DPA. Buyers who have a disability, or whose household includes a member with a disability, can qualify for the HomeChoice program: up to $15,000 at 1% simple interest. Both are paired with a WSHFC first mortgage and can be used alongside Home Advantage or House Key, layering additional help on top of the primary assistance.

City and county programs that layer on top of state help

Washington's geographic-specific programs allow buyers within certain city or county boundaries to access significantly higher assistance amounts. These can be stacked with WSHFC programs when they're compatible, which can significantly increase total assistance available.

Seattle and East King County programs with higher caps

Seattle's down payment assistance program offers up to $55,000 at 4% simple interest, repaid upon sale or refinance. Eligibility requires purchasing within Seattle city limits and earning at or below 80% of the area median income. The Seattle Office of Housing also partners with HomeSight and Parkview Services, allowing eligible buyers to layer additional assistance on top. (Confirm current terms and partner requirements at the Seattle Office of Housing.)

Buyers in East King County member communities can access the ARCH program: up to $30,000 at 4% simple interest. These programs operate separately from WSHFC but can be paired with a WSHFC first mortgage. Bellingham buyers have access to up to $40,000 at 3%. A Commission-trained lender confirms compatibility before any offer is written. (Verify current program terms at the ARCH and City of Bellingham program pages.)

What Snohomish County first-time buyers can access

Snohomish County doesn't have a standalone high-cap city program the way Seattle does, but buyers here still benefit meaningfully from statewide WSHFC first-time buyer assistance. The needs-based DPA income limit of $164,400 applies to Snohomish County, the same higher threshold as King County, which opens eligibility to a broader range of local households.

Given the county's home prices and buyer demographics, those programs are a practical tool for a wide range of first-time buyers. Pilchard Properties works with buyers across Everett, Edmonds, and surrounding Snohomish County communities, helping clients identify which programs fit their situation before they begin shopping for homes. Learn more about local down payment expectations in our article How Much Down Payment Do You Actually Need to Buy a Home in Snohomish County?.

Stacking programs: how buyers maximize their total assistance

When programs are compatible, buyers can layer a city or county program on top of a WSHFC first mortgage and down payment assistance. A Snohomish County buyer using Home Advantage's 3% DPA alongside the $10,000 needs-based second mortgage receives meaningful combined help without a single additional monthly payment. A Commission-trained lender coordinates all of this. Buyers shouldn't try to combine programs without that guidance, not every combination is permitted.

How to apply for first-time home buyer assistance in Washington State

Complete the homebuyer education course before anything else

Most WSHFC programs require a 5-hour WSHFC-approved homebuyer education course from an approved provider. This is the first step, and it must happen before applying for down payment assistance. The online self-guided version is available through eHomeAmerica at $50 per borrower. Each borrower on the loan must register separately. Once completed, you receive a certificate that becomes part of your application package.

Some programs, particularly those through the Seattle Office of Housing, also require one-on-one housing counseling in addition to the course. Check the specific requirements for any program you're applying to before assuming the course alone is sufficient.

Documents to have ready before your lender call

Gathering documents before reaching out to a lender speeds up the pre-approval timeline considerably. You'll need recent tax returns, W-2s or current pay stubs, proof of identity and citizenship or legal residency, and your homebuyer education completion certificate. For the Covenant program, add historical documentation proving pre-1968 family roots in Washington State. The lender coordinates submission to WSHFC on your behalf, but you're responsible for having the materials organized and ready to provide.

Finding a participating lender and getting pre-approved

Buyers must work with a WSHFC Commission-trained lender to access these programs. The Here to Home portal at heretohome.org lists participating lenders by county with direct contact information. Lenders active in WSHFC programs include NFM Lending, First Fed, New American Funding, and Fairway Independent Mortgage, among others on the Commission's approved list.

The lender pre-approves you for the mortgage, confirms your DPA eligibility, and submits all documentation to WSHFC before any offers are written. For the Covenant program, that authorization step is especially critical and must happen before you begin house-hunting.

Why local expertise makes a real difference in this process

What a program-literate agent actually does for first-time buyers

There's a meaningful gap between knowing programs exist and knowing how to use them in practice. An agent familiar with Washington homeownership assistance helps you understand income limits before you write an offer on a home that doesn't work within those constraints. They connect you with participating lenders early, structure offers with DPA timelines in mind, and prevent the common, costly mistake of discovering program requirements after you're already under contract.

A knowledgeable local agent also understands which lenders move efficiently in your county, which programs see the most use locally, and how to keep a first-time buyer's offer competitive in a market where timing affects outcomes.

How Pilchard Properties supports first-time buyers in Snohomish County

Pilchard Properties is a Snohomish County team built around exactly this kind of work. Broker Renee Pilchard and her team guide first-time buyers across Everett, Edmonds, Snohomish, and surrounding communities through the full range of WSHFC programs, helping them identify the right combination of assistance, connect with effective local lenders, and write competitive offers in a market where speed matters.

The team's multi-agent structure means buyers always have a responsive, knowledgeable agent available for showings and questions, without the delays that come from working with a single overextended agent. If you're beginning to explore homes in Snohomish County, starting with a team that understands these programs is a practical first move, not an optional one. For a local perspective on getting started, see our First-Time Home Buyer Guide in Lake Stevens, WA (2026 Edition).

The path is more supported than most buyers think

First-time home buyer assistance in Washington State is more extensive and accessible than most buyers realize going in. The programs are real, the eligibility rules are specific but learnable, and the assistance can meaningfully reduce the upfront cost of buying a home.

The steps are straightforward: take the WSHFC-approved education course, calculate your gross household income against current program limits, find a Commission-trained lender through heretohome.org, and work with a local agent who understands how these programs operate in your specific county. Each of those steps builds on the last.

If you want to explore first-time home buyer assistance Washington State options, start with the WSHFC-approved lender list at heretohome.org, and reach out to Pilchard Properties to understand which programs make sense for your situation before you begin your search. Many buyers are unaware these options exist; the ones who find out early are the ones who use them.